UIN: NIAHLIP24123V032324 Page 1 of 24

NEW INDIA ASHA KIRAN POLICY

THE NEW INDIA ASSURANCE CO. LTD.

REGISTERED & HEAD OFFICE: 87, MAHATMA GANDHI ROAD, MUMBAI 400001

NEW INDIA ASHA KIRAN POLICY- PROSPECTUS

We welcome You as Our Customer. This document explains how the NEW INDIA ASHA KIRAN POLICY

could provide value to You. In the document the word ‘You’, ‘Your’ means the all the members covered

under the Policy. ‘We’, ‘Our’, ‘Us’ means The New India Assurance Co. Ltd.

New India Asha Kiran is a Policy designed to cover Hospitalisation expenses of the family and Personal

Accident for Parents.

1. WHO CAN TAKE THIS POLICY?

THIS POLICY IS DESIGNED TO THE PARENTS WITH ONLY GIRL CHILDREN. This insurance is available to

persons between the age of 18 years and 65 years. Daughter(s) from 3 months up to 25 years can be

covered provided they are financially dependent on the parents and one or both parents are covered

simultaneously. The upper age limit will not apply to mentally challenged daughter(s) and unmarried

dependent daughter(s). The persons beyond 65 years can continue their insurance provided they are

insured under the Policy with us without any break

Midterm inclusion is allowed for Newly Born Daughter (after completing 3 months) by charging pro-rata

Premium for the remaining period of the Policy.

2. CAN I COVER MY FAMILY MEMBERS IN ONE POLICY?

Yes. You can cover the entire family under a Single Sum Insured (Floater). The members of the family who

could be covered under the Policy are:

a) Proposer

b) Proposer’s Spouse

c) Proposer’s Dependent Daughter (Maximum Two)

Minimum two members, with at least one daughter, are required in this policy. This policy cannot be given

to a single person. Maximum four members can be covered in a single policy. Midterm inclusion is allowed

only for new born 2nd baby girl child on payment of pro - rata additional premium.

3. WHAT DOES THE POLICY COVER?

This Policy is designed to give You and Your family, protection against unforeseen Hospitalization expenses

and Accident cover to Proposer and Spouse.

4. WHAT ARE THE EXPENSES COVERED UNDER THIS POLCY?

Our liability for all claims admitted during the Period of Insurance in respect of all Insured Persons

shall not exceed the Sum Insured. Subject to this, for each claim We will reimburse the following

UIN: NIAHLIP24123V032324 Page 2 of 24

NEW INDIA ASHA KIRAN POLICY

Reasonable and Customary and Medically Necessary Expenses admissible as per the terms and

conditions of the Policy:

(a)

Room rent, Boarding, DMO / RMO / CMO / RMP Charges, Nursing (Including Injection /

Drugs and Intra venous fluid administration expenses), not exceeding 1% of the Sum

Insured per day.

(b)

Intensive Care Unit (ICU) / Intensive Cardiac Care Unit (ICCU), Intensivist charges, Monitor

and Pulse Oxymeter expenses, not exceeding 2% of the Sum Insured per day.

(c)

Associate Medical Expenses; such as Professional fees of Surgeon, Anaesthetist,

Consultant, Specialist; Anaesthesia, Operating Theatre Charges and Procedure Charges

such as Dialysis, Chemotherapy, Radiotherapy & similar medical expenses related to the

treatment.

(d)

Cost of Pharmacy and Consumables, Cost of Implants and Medical Devices and Cost of

Diagnostics.

(e)

Pre-Hospitalization Medical Expenses, not exceeding thirty days

(f)

Post-Hospitalization Medical Expenses, not exceeding sixty days

(g)

Proportionate Deduction is applicable on the Associate Medical Expenses, if the Insured

Person opts for a higher Room than his eligible category. It shall be effected in the same

proportion as the eligible rate per day bears to the actual rate per day of Room Rent.

However, it is not applicable on

1. Cost of Pharmacy and Consumables

2. Cost of Implants and Medical Devices

3. Cost of Diagnostics.

Proportionate Deduction shall also not be applied in respect of Hospitals which do not

follow differential billing or for those expenses in which differential billing is not adopted

based on the room category, as evidenced by the Hospital’s schedule of charges / tariff.

Note:

(h) MEDICAL EXPENSES INCURRED UNDER TWO POLICY PERIODS:

If the claim event falls within two policy periods, the claims shall be paid taking into

consideration the available Sum Insured of the expiring Policy only. Sum Insured of the

Renewed Policy will not be available for the Hospitalisation (including Pre & Post Hospitalisation

Expenses), which has commenced in the expiring Policy. Claim shall be settled on per event

basis.

(i) MEDICAL EXPENSES FOR ORGAN TRANSPLANT:

If treatment involves Organ Transplant to Insured Person, then We will also pay Hospitalisation

Expenses (excluding cost of organ) incurred on the donor, provided Our liability towards

expenses incurred on the donor and the insured recipient shall not exceed the aggregate of the

Sum Insured, if any, of the Insured Person receiving the organ.

UIN: NIAHLIP24123V032324 Page 3 of 24

NEW INDIA ASHA KIRAN POLICY

(j) Dental Treatment (Inpatient): We will cover for medical expenses incurred towards dental

treatment done under anaesthesia necessitated due to an accident/injury/illness requiring

Hospitalization as Inpatient treatment.

LIMIT ON PAYMENT FOR CATARACT

Our liability for payment of any claim within the Period of Insurance, relating to Cataract for

each eye shall not exceed 10% of the Sum Insured or Rs. 50,000, whichever is less.

TREATMENTS UNDER AYURVEDIC/HOMEOPATHIC/UNANI SYSTEMS

Our liability for expenses incurred for Ayurvedic/Homeopathic/Unani treatments shall not

exceed 25% of the Sum Insured in respect of all such treatments admitted during the Period

of Insurance, provided the treatment for Illness or Injury, is taken in any AYUSH Hospital.

HOSPITAL CASH

We will pay Hospital Cash at the rate of 0.1% of the Sum Insured, for each day of Hospitalisation,

admissible under the Policy. The payment under this Clause for Any One Illness shall not exceed

1% of the Sum Insured. The payment under this Clause is applicable only where the period of

Hospitalization exceeds twenty-four hours.

CRITICAL CARE BENEFIT

If during the Period of Insurance any Insured Person discovers that he or she is suffering from

any Critical Illnesses as defined under 2.8 of the Policy Clause, which results in a claim admissible

under this Policy, 10% of the Sum Insured would be paid as Critical Care Benefit along with the

admissible claim amount.

Critical Care Benefit is payable only once in the life time of each Insured Person and is not

applicable to any Insured Persons for whom it is a Pre- Existing Condition/Disease.

Any payment under this Clause would be in addition to the Sum Insured and shall not deplete

the Sum Insured.

PAYMENT OF AMBULANCE CHARGES

We will pay You the charges for Ambulance services not exceeding 1% of the Sum Insured per

Insured event, Medically Necessarily incurred for shifting any Insured Person to Hospital for

admission in Emergency Ward or ICU, or from one Hospital to another Hospital for better

medical facilities.

PAYMENTS ONLY IF INCLUDED IN HOSPITAL BILL

No payment shall be made for any Hospitalisation expenses incurred, unless they form part of

the Hospital Bill. However, the bills raised by Surgeon, Anaesthetist directly and not included in

the Hospital Bill shall be paid provided a numbered Bill is produced in support thereof, for an

UIN: NIAHLIP24123V032324 Page 4 of 24

NEW INDIA ASHA KIRAN POLICY

amount not exceeding Rs. Ten thousand, where such payment is made in cash and for an

amount not exceeding Rs. Twenty thousand, where such payment is made by cheque.

TREATMENT FOR CONGENITAL DISEASES

Congenital Internal Disease or Defects or anomalies shall be covered after twenty-four months

of Continuous Coverage. if it was unknown to You or to the Insured Person at the

commencement of such Continuous Coverage. Exclusion for Congenital Internal Disease or

Defects or Anomalies would not apply to a New Born Baby during the year of Birth and also

subsequent renewals, if Premium is paid for such New Born Baby and the renewals are effected

before or within thirty days of expiry of the Policy.

Congenital External Disease or Defects or anomalies shall be covered after forty-eight months

of Continuous Coverage, but such cover for Congenital External Disease or Defects or anomalies

shall be limited to 10% of the average Sum Insured in the preceding four years.

OPTIONAL COVER I: NO PROPORTIONATE DEDUCTION

On payment of additional Premium as mentioned in Schedule, it is hereby agreed and declared

that Clause 3.1(g) stands deleted for the members covered in the Policy as stated in the

Schedule.

You shall continue to bear the differential between actual and eligible Room Rent.

OPTIONAL COVER II: MATERNITY EXPENSES BENEFIT

On the payment of additional Premium as mentioned in Schedule, it is hereby agreed and

declared that Clause 4.4.15 stands deleted for Insured Person as mentioned in the Schedule.

Our liability for claim admitted for Maternity shall not exceed 10% of the average Sum Insured

of the Insured Person in the preceding three years. This Optional Cover is available for Sum

Insured 5 L & above.

Special conditions applicable to Maternity Expenses Benefit:

i These Benefits are admissible only if the expenses are incurred in Hospital as inpatients in

India.

ii A waiting period of thirty-six months is applicable, from the date of opting this cover, for

payment of any claim relating to normal delivery or caesarian section or abdominal

operation for extra uterine pregnancy. The waiting period may be relaxed only in case of

miscarriage or abortion induced by accident or other medical emergency.

iii Claim in respect of delivery for only first two children and / or surgeries associated

therewith will be considered in respect of any one Insured Person covered under the

Policy or any renewal thereof.

iv Expenses incurred in connection with voluntary medical termination of pregnancy during

the first 12 weeks from the date of conception are not covered.

UIN: NIAHLIP24123V032324 Page 5 of 24

NEW INDIA ASHA KIRAN POLICY

Pre-natal and post-natal expenses are not covered unless admitted in Hospital and treatment

is taken there.

OPTIONAL COVER III: REVISION IN LIMIT OF CATARACT

This optional cover, if opted, will be in addition to limit specified in Clause 3.2 of the Policy

Clause. This Optional Cover is available for Sum Insured 8 L & above.

On payment of additional Premium as mentioned in Schedule, it is declared and agreed that

following additional amount for Cataract shall become payable but not exceeding the actual

expenses incurred:

Sum Insured

Additional Cataract limit

Rs. 8,00,000

Rs. 80,000

Rs. 10,00,000

Rs. 1,00,000

Rs. 12,00,000

Rs. 1,20,000

Rs. 15,00,000

Rs. 1,50,000

Note: Benefit of this cover will be available after the expiry of thirty-six months from the date

of opting this cover.

OPTIONAL COVER IV: NON-MEDICAL ITEMS (CONSUMABLES)

On payment of additional Premium as mentioned in Schedule, it is declared and agreed that

items listed in Annexure II (List 1) shall become payable up to Rs. 15,000/- in a policy period.

This Optional Cover is available for Sum Insured of 8 L & above.

Once this optional cover is opted and a claim has been admitted under the policy, You cannot

opt out of this optional cover.

SPECIFIC COVERAGES:

a) Artificial life maintenance, including life support machine use, where such treatment will not

result in recovery or restoration of normal state of Health under any circumstances. We cover

the expenses up to 10% of the Sum Insured and for a maximum of 15 days per policy period

for covered illness. This sub limit is applicable only for person who is declared to be in a

vegetative state as certified by the treating medical practitioner.

b) Puberty and Menopause related Disorders: Treatment for any symptoms, Illness,

complications arising due to physiological conditions associated with Puberty, Menopause

such as menopausal bleeding or flushing is covered only as Inpatient procedure after 24

months of continuous coverage. This cover will have a sub-limit of up to 25% of Sum Insured

per policy period.

c) Age Related Macular Degeneration (ARMD) is covered after 48 months of continuous

coverage only for Intravitreal Injections and anti - VEGF medication. This cover will have a sub-

limit of 10% of Sum Insured, maximum upto Rs. 75,000 per policy period.

UIN: NIAHLIP24123V032324 Page 6 of 24

NEW INDIA ASHA KIRAN POLICY

d) Genetic diseases or disorders are covered with a sub-limit of 25% of Sum Insured per policy

period with 48 months waiting periods.

Note: For the coverages defined in (a) to (d) above, waiting period's, if any, shall be applicable

afresh i.e. for both New and Existing Policyholders w.e.f 1

st

October 2020. Coverage for such

Illness or procedures shall only be available after completion of the said waiting periods.

e) Treatment of Mental Illness: The Company shall indemnify the Medical Expenses incurred

towards treatment of Mental Illness subject to the condition that Treatment shall be

undertaken at a Hospital categorized as Mental Health Establishment or at a Hospital with a

specific department for Mental Illness, under a Medical Practitioner qualified as Mental

Health Professional.

The following Mental Illnesses are covered after completion of 48 months of Continuous

Coverage with a sub-limit up to 25% of Sum Insured per policy period.

ICD Code

ICD Code Description

F01-F09

Mental disorders due to known physiological conditions

F10-F19

Mental and behavioral disorders due to psychoactive substance use

F20-F29

Schizophrenia, schizotypal, delusional, and other non-mood psychotic disorders

F60-F69

Disorders of adult personality and behavior

F70-F79

Intellectual disabilities

Exclusion: Any kind of Psychological counselling, cognitive/ family/ group/ behaviour/ palliative

therapy or psychotherapy shall not be covered.

COVERAGE FOR MODERN TREATMENTS or PROCEDURES: The following procedures will be

covered (wherever medically indicated) either as in patient or as part of day care treatment in

a hospital up to the limit specified against each procedure during the policy period.

Treatment or Procedure

Limit (Per Policy Period)

Uterine Artery Embolization and HIFU (High intensity

focused ultrasound)

Up to 20% of Sum Insured subject to

Maximum Rs. 1 Lakh

Balloon Sinuplasty.

Up to 20% of Sum Insured subject to

Maximum Rs. 1 Lakh

Deep Brain stimulation.

Up to 50% of Sum Insured subject to M

maximum Rs. 1.5 Lakh

Oral chemotherapy.

Up to 10% of Sum Insured subject to

Maximum Rs. 50,000.

Immunotherapy- Monoclonal Antibody to be given as

injection.

Up to 25% of Sum Insured subject to

Maximum Rs 1 Lakh.

Intravitreal injections.

Up to 10% of Sum Insured subject to

Maximum Rs.30,000.

Robotic surgeries.

Up to 50% of Sum Insured subject to

Maximum Rs. 2 Lakh.

Stereotactic radio surgeries.

Up to 50% of Sum Insured subject to

Maximum Rs. 1.5 Lakh.

UIN: NIAHLIP24123V032324 Page 7 of 24

NEW INDIA ASHA KIRAN POLICY

Bronchial Thermoplasty.

Up to 50% of Sum Insured subject to

Maximum Rs. 1.5 Lakh.

Vaporisation of the prostrate (Green laser treatment or

holmium laser treatment).

Up to 50% of Sum Insured subject to

Maximum Rs. 1.5 Lakh.

IONM - (Intra Operative Neuro Monitoring).

Up to 10% of Sum Insured subject to

Maximum Rs. 25,000.

Stem cell therapy: Hematopoietic stem cells for bone

marrow transplant for haematological conditions to be

covered.

Up to 50% of Sum Insured subject to

Maximum Rs. 1.5 Lakh.

SECTION II: PERSONAL ACCIDENT (APPLICABLE TO PROPOSER AND SPOUSE)

If the Proposer and/or Spouse shall sustain any bodily Injury resulting solely and directly from

Accident then We shall pay to dependent daughter(s) as specified in the schedule, the sum

hereinafter set forth that is to say:

If such Injury shall within twelve calendar months of its occurrence be the sole and direct cause of

Coverage

Compensation

Death of

Proposer or Spouse

100% of Sum Insured

Proposer and Spouse

200% of Sum Insured

Permanent Total Disablement of

Proposer or Spouse

100% of Sum Insured

Proposer and Spouse

200% of Sum Insured

Loss of both eyes / Loss of both limbs /

Loss of one limb and one eye of

Proposer or Spouse

100% of Sum Insured

Proposer and Spouse

200% of Sum Insured

Loss of one limb / one eye of

Proposer or Spouse

50% of Sum Insured

Proposer and Spouse

100% of Sum Insured

If the dependent daughter(s) specified in the schedule, is/are minor at the time of claim, then

the money will be deposited as fixed deposit in a Nationalized Bank, to be paid to daughter(s)

after attaining majority.

Note: The Company shall not be liable under this Policy for Compensation under more than

one of the sub-clauses, as mentioned above, in respect of same Injury or disablement.

In the event of unfortunate death of all the Insured Persons specified in the policy, no such

benefits shall be payable under this Section.

Any payment under this Clause would be in addition to the Sum Insured and shall not deplete

the Sum Insured.

UIN: NIAHLIP24123V032324 Page 8 of 24

NEW INDIA ASHA KIRAN POLICY

5. WHAT IS HOSPITAL CASH BENEFIT?

This policy provides for payment of Hospital Cash at the rate of 0.1% of Sum Insured per day of

Hospitalisation. This benefit will be given in every case of admissible claim and for each member. This

benefit is applicable only where Hospitalisation exceeds twenty four consecutive hours.

The total payment for Any One Illness shall not exceed 1% of the Sum Insured. This benefit shall be directly

given by TPA/underwriting office, as the case may be.

6. WHAT IS CRITICAL CARE BENEFIT?

If during the Period of Insurance any Insured Person discovers that he/she is suffering from any Critical

Illnesses as listed below and as defined under 2.8 of the Policy Clause, which results in a claim admissible

under this Policy, we will pay flat 10% of Sum Insured as additional benefit i.e. over and above the

admissible claim:

a Cancer of Specified severity

b First Heart attack of specified severity

c Open chest CABG

d Open Heart replacement or repair of Heart valves

e Coma of specified severity

f Kidney failure requiring regular dialysis

g Stroke resulting in permanent symptoms

h Major organ / bone marrow transplant

i Permanent paralysis of limbs

j Motor neurone disease with permanent symptoms

k Multiple sclerosis with persisting symptoms

Any payment under this clause would be in addition to the Sum Insured and shall not deplete the Sum

Insured. This benefit will be paid once in lifetime of any Insured Person. This benefit is not applicable for

those Insured Persons for whom it is a pre-existing disease.

7. IS PRE-ACCEPTANCE MEDICAL CHECK-UP REQUIRED?

Pre-acceptance test is required for all the members entering after the age of 50 for the first time. A person

also needs to undergo this pre-acceptance medical check-up if he has an adverse medical history. The cost

of this check-up will be borne by the proposer. But if the proposal is accepted, then 50% of the cost of this

check-up will be reimbursed to the proposer. List of Medical Tests required are as below.

CBC

Serum HDL

Blood Sugar Fasting & Post Prandial

Routine Urine Examination (RUE)

SGPT

Resting ECG

SGOT

X RAY Chest PA View

Serum Cholesterol

Physician Check Up

Serum Triglycerides

Eye Check Up For Cataract & Glaucoma

UIN: NIAHLIP24123V032324 Page 9 of 24

NEW INDIA ASHA KIRAN POLICY

8. DOES IT COVER ALL CASES OF HOSPITALISATION?

No claim will be payable under this Policy for the following:

STANDARD EXCLUSIONS

PRE-EXISTING DISEASES (Code- Excl01)

a. Expenses related to the treatment of a pre-existing Disease (PED) and its direct complications

shall be excluded until the expiry of 48 months of continuous coverage after the date of inception

of the first policy with us.

b. In case of enhancement of Sum Insured the exclusion shall apply afresh to the extent of Sum

Insured increase.

c. If the Insured Person is continuously covered without any break as defined under the portability

norms of the extant IRDAI (Health Insurance) Regulations then waiting period for the same would

be reduced to the extent of prior coverage.

d. Coverage under the policy after the expiry of 48 months for any pre-existing disease is subject to

the same being declared at the time of application and accepted by us.

SPECIFIC WAITING PERIOD (Code- Excl02)

a. Expenses related to the treatment of the following listed conditions, surgeries / treatments shall

be excluded until the expiry of Ninety Days / 24 / 48 months of continuous coverage, as may be

the case after the date of inception of the first policy with the insurer. This exclusion shall not be

applicable for claims arising due to an accident.

b. In case of enhancement of sum insured the exclusion shall apply afresh to the extent of sum

insured increase.

c. If any of the specified disease/procedure falls under the waiting period specified for preexisting

diseases, then the longer of the two waiting periods shall apply.

d. The waiting period for listed conditions shall apply even if contracted after the policy or declared

and accepted without a specific exclusion.

e. If the Insured Person is continuously covered without any break as defined under the applicable

norms on portability stipulated by IRDAI, then waiting period for the same would be reduced to

the extent of prior coverage.

i. 90 Days Waiting Period

1. Diabetes Mellitus

2. Hypertension

3. Cardiac Conditions

ii. 24 Months waiting period

1. All internal and external benign tumours, cysts, polyps of any kind, including benign breast

lumps

UIN: NIAHLIP24123V032324 Page 10 of 24

NEW INDIA ASHA KIRAN POLICY

2. Benign ear, nose, throat disorders

3. Benign prostate hypertrophy

4. Cataract and age related eye ailments

5. Gastric/ Duodenal Ulcer

6. Gout and Rheumatism

7. Hernia of all types

8. Hydrocele

9. Non Infective Arthritis

10. Piles, Fissures and Fistula in anus

11. Pilonidal sinus, Sinusitis and related disorders

12. Prolapse inter Vertebral Disc and Spinal Diseases unless arising from accident

13. Skin Disorders

14. Stone in Gall Bladder and Bile duct, excluding malignancy

15. Stones in Urinary system

16. Treatment for Menorrhagia/Fibromyoma, Myoma and Prolapsed uterus

17. Varicose Veins and Varicose Ulcers

18. Puberty and Menopause related Disorders

19. Internal Congenital Diseases

iii. 48 Months waiting period

1. Joint Replacement due to Degenerative Condition

2. Age-related Osteoarthritis & Osteoporosis

3. Treatment of mental illness

4. Age Related Macular Degeneration (ARMD)

5. Genetic diseases or disorders

6. External Congenital Diseases

FIRST THIRTY DAYS WAITING PERIOD (Code- Excl03)

a. Expenses related to the treatment of any illness within 30 days from the first policy

commencement date shall be excluded except claims arising due to an accident, provided the

same are covered.

b. This exclusion shall not, however, apply if the Insured Person has Continuous Coverage for more

than twelve months.

c. The within referred waiting period is made applicable to the enhanced sum insured in the event

of granting higher sum insured subsequently.

EXCLUSIONS

The Company shall not be liable to make any payment under the policy, in respect of any expenses

incurred in connection with or in respect of:

INVESTIGATION & EVALUATION (Code- Excl04)

a. Expenses related to any admission primarily for diagnostics and evaluation purposes.

UIN: NIAHLIP24123V032324 Page 11 of 24

NEW INDIA ASHA KIRAN POLICY

b. Any diagnostic expenses which are not related or not incidental to the current diagnosis and

treatment

REST CURE, REHABILITATION AND RESPITE CARE (Code- Excl05) Expenses related to any admission

primarily for enforced bed rest and not for receiving treatment. This also includes:

a. Custodial care either at home or in a nursing facility for personal care such as help with activities

of daily living such as bathing, dressing, moving around either by skilled nurses or assistant or

non-skilled persons.

b. Any services for people who are terminally ill to address physical, social, emotional and spiritual

needs.

OBESITY/ WEIGHT CONTROL (Code- Excl06) Expenses related to the surgical treatment of obesity that

does not fulfil all the below conditions:

a. Surgery to be conducted is upon the advice of the Doctor

b. The surgery/Procedure conducted should be supported by clinical protocols

c. The member has to be 18 years of age or older and

d. Body Mass Index (BMI);

1. greater than or equal to 40 or

2. greater than or equal to 35 in conjunction with any of the following severe comorbidities

following failure of less invasive methods of weight loss:

i. Obesity-related cardiomyopathy

ii. Coronary heart disease

iii. Severe Sleep Apnea iv. Uncontrolled Type2 Diabetes

CHANGE-OF-GENDER TREATMENTS (Code- Excl07)

Expenses related to any treatment, including surgical management, to change characteristics of the

body to those of the opposite sex.

COSMETIC OR PLASTIC SURGERY (Code- Excl08)

Expenses for cosmetic or plastic surgery or any treatment to change appearance unless for

reconstruction following an Accident, Burn(s) or Cancer or as part of medically necessary treatment to

remove a direct and immediate health risk to the insured. For this to be considered a medical necessity,

it must be certified by the attending Medical Practitioner.

HAZARDOUS OR ADVENTURE SPORTS (Code- Excl09)

Expenses related to any treatment necessitated due to participation as a professional in hazardous or

adventure sports, including but not limited to, para-jumping, rock climbing, mountaineering, rafting,

motor racing, horse racing or scuba diving, hand gliding, sky diving, deep-sea diving.

BREACH OF LAW (Code- Excl10)

Expenses for treatment directly arising from or consequent upon any Insured Person committing or

attempting to commit a breach of law with criminal intent.

EXCLUDED PROVIDERS (Code-Excl11)

Expenses incurred towards treatment in any hospital or by any Medical Practitioner or any other

provider specifically excluded by the Insurer and disclosed in its website / notified to the policyholders

are not admissible. However, in case of life-threatening situations or following an accident, expenses

up to the stage of stabilization are payable but not the complete claim.

Treatment for, Alcoholism, drug or substance abuse or any addictive condition and consequences

thereof. (Code- Excl12)

UIN: NIAHLIP24123V032324 Page 12 of 24

NEW INDIA ASHA KIRAN POLICY

Treatments received in health hydros, nature cure clinics, spas or similar establishments or private

beds registered as a nursing home attached to such establishments or where admission is arranged

wholly or partly for domestic reasons. (Code- Excl13)

Dietary supplements and substances that can be purchased without prescription, including but not

limited to Vitamins, minerals and organic substances unless prescribed by a medical practitioner as

part of hospitalization claim or day care procedure. (Code- Excl14)

REFRACTIVE ERROR (Code- Excl15)

Expenses related to the treatment for correction of eye sight due to refractive error less than

7.5 dioptres.

UNPROVEN TREATMENTS (Code- Excl16)

Expenses related to any unproven treatment, services and supplies for or in connection with any

treatment. Unproven treatments are treatments, procedures or supplies that lack significant medical

documentation to support their effectiveness.

STERILITY AND INFERTILITY (Code- Excl17)

Expenses related to sterility and infertility. This includes:

a. Any type of contraception, sterilization

b. Assisted Reproduction services including artificial insemination and advanced reproductive

technologies such as IVF, ZIFT, GIFT, ICSI

c. Gestational Surrogacy

d. Reversal of sterilization

MATERNITY EXPENSES (Code - Excl18)

a. Medical treatment expenses traceable to childbirth (including complicated deliveries and

caesarean sections incurred during hospitalization) except ectopic pregnancy;

b. Expenses towards miscarriage (unless due to an accident) and lawful medical termination of

pregnancy during the policy period.

SPECIFIC EXCLUSIONS

Acupressure, acupuncture, magnetic therapies.

Any expenses incurred on Domiciliary Hospitalization.

Service charges, Surcharges, Luxury Tax, Admission fees, Registration fees, Record Charges and

Telephone Charges levied by the Hospital.

Bodily Injury or Illness due to willful or deliberate exposure to danger (except in an attempt to save

human life), intentional self-inflicted Injury and attempted suicide.

Circumcision unless Medically Necessary or as may be necessitated due to an Accident.

Convalescence and General debility.

Cost of braces, equipment or external prosthetic devices, eyeglasses, Cost of spectacles and contact

lenses, hearing aids including cochlear implants.

External Medical / Non-medical equipment used for diagnosis and/or treatment including

CPAP/BIPAP, Oxygen Concentrator, Infusion pump , Ambulatory devices (walker, crutches, Collars,

Caps, Splints, Elasto crepe bandages, external orthopaedic pads) and sub cutaneous insulin pump,

Diabetic foot wear, Glucometer / Thermometer and equipment, which is subsequently used at home

and outlives the use and life of the Insured Person.

Naturopathy Treatment.

Nuclear, chemical or biological attack or weapons, contributed to, caused by, resulting from or from

any other cause or event contributing concurrently or in any other sequence to the loss, claim or

expense. For the purpose of this exclusion:

UIN: NIAHLIP24123V032324 Page 13 of 24

NEW INDIA ASHA KIRAN POLICY

a. Nuclear attack or weapons means the use of any nuclear weapon or device or waste or

combustion of nuclear fuel or the emission, discharge, dispersal, release or escape of fissile/

fusion material emitting a level of radioactivity capable of causing any Illness, incapacitating

disablement or death.

b. Chemical attack or weapons means the emission, discharge, dispersal, release or escape of any

solid, liquid or gaseous chemical compound which, when suitably distributed, is capable of

causing any Illness, incapacitating disablement or death.

c. Biological attack or weapons means the emission, discharge, dispersal, release or escape of any

pathogenic (disease producing) micro-organisms and/or biologically produced toxins (including

genetically modified organisms and chemically synthesized toxins) which are capable of causing

any Illness, incapacitating disablement or death.

Stem cell implantation/Surgery for other than those treatments mentioned in clause 3.14.12 of the

Policy Clause.

Treatments such as Rotational Field Quantum Magnetic Resonance (RFQMR), External Counter

Pulsation (ECP), Enhanced External Counter Pulsation (EECP), Hyperbaric Oxygen Therapy.

Treatment taken outside the geographical limits of India.

Vaccination and/or inoculation.

War (whether declared or not) and war like occurrence or invasion, acts of foreign enemies, hostilities,

civil war, rebellion, revolutions, insurrections, mutiny, military or usurped power, seizure, capture,

arrest, restraints and detainment of all kinds.

Payment or compensation in respect of death, Injury or disablements directly or indirectly arising out

of or contributed to or traceable to any disability already existing on the date of commencement of

this policy.

Procedures / treatments usually done in outpatient department are not payable under the Policy even

if converted as an in-patient in the Hospital for more than twenty-four consecutive hours.

Change of treatment from one system to another unless recommended by the consultant/

Hospital under which the treatment is taken.

9. WHAT IS A PRE EXISTING DISEASE?

The term Pre-existing condition/disease is defined in the Policy. It means any condition, ailment, Injury or

Illness

a. That is/are diagnosed by a physician within 48 months prior to the effective date of the Policy issued

by Us and its reinstatement or

b. For which medical advice or treatment was recommended by, or received from, a physician within 48

months prior to the effective date of the Policy or its reinstatement.

10. IS HOSPITALISATION ALWAYS NECESSARY TO GET A CLAIM?

Yes. Unless the Insured Person is Hospitalised for a condition warranting Hospitalisation, no claim is payable

under the Policy. The Policy does not cover outpatient treatments.

In case of Death Claim, Hospitalisation is not required but the death certificate, post mortem

report and police report is required.

UIN: NIAHLIP24123V032324 Page 14 of 24

NEW INDIA ASHA KIRAN POLICY

In case of Disability, Hospitalisation is not required but medical certificate certifying the

disablement and police report (if any) is required

11. HOW LONG DOES THE INSURED PERSON NEED TO BE HOSPITALISED?

The Policy pays only where the Hospitalisation is for more than twenty-four hours. But for certain

treatments specified in the Policy, period of stay at the Hospital could be less than twenty-four hours.

12. WHAT ARE THE DAY CARE TREATMENTS COVERED UNDER THIS POLICY?

Day Care Procedures shall be as per Annexure 1 of the Policy Clause.

13. WHAT DO I NEED TO DO IF ANYBODY COVERED IN THE POLICY NEEDS TO GET HOSPITALISED?

For Hospitalization Claim

Upon the happening of any event which may give rise to a claim under the policy, please immediately

intimate the TPA named in the schedule with all the details such as name of the Hospital, details of

treatment, patient name, policy number etc.

In case of emergency Hospitalisation, this information needs to be given to the TPA, within 24 hours from

the time of Hospitalisation.

For Personal Accident:

In case of death claim:

Nominee as specified in the policy schedule should immediately notify the policy issuing office

Submit the claim form along with death certificate, post mortem report, police report and original

policy.

In case of Injury claim:

Notify the policy issuing office immediately.

Submit Police report if any.

Submit claim form along with medical certificate certifying the disablement.

These are important conditions that you need to comply with.

14. WHAT ARE THE AMBULANCE CHARGES PAID UNDER THIS POLICY?

Company will pay ambulance charges up to 1% of SI or actual whichever is less. These charges are available

in case of emergency extraction from anywhere to Hospital or Hospital to Hospital.

15. IS PAYMENT AVAILABLE FOR EXPENSES INCURRED BEFORE HOSPITALISATION?

Yes. Medical Expenses incurred immediately before, but not exceeding thirty days, the Insured Person is

Hospitalised will be paid, provided that:

i. Such Medical Expenses are incurred for the same condition for which the Insured Person’s

Hospitalisation was required, and

UIN: NIAHLIP24123V032324 Page 15 of 24

NEW INDIA ASHA KIRAN POLICY

ii. The In-patient Hospitalisation claim for such Hospitalisation is admissible by Us.

16. IS PAYMENT AVAILABLE FOR EXPENSES INCURRED AFTER HOSPITALISATION?

Yes. Medical Expenses incurred immediately after, but not exceeding sixty days, the Insured Person is

discharged from the Hospital will be paid, provided that:

i. Such Medical Expenses are incurred for the same condition for which the Insured Person’s

Hospitalisation was required, and

ii. The In-patient Hospitalisation claim for such Hospitalisation is admissible by Us.

17. IS THERE A LIMIT TO WHAT THE COMPANY WILL PAY FOR HOSPITALISATION?

Yes. We will pay Hospitalisation expenses upto a limit, known as Sum Insured. In cases where the Insured

Person was Hospitalised more than once, the total of all amounts paid

a) for all cases of Hospitalisation,

b) expenses paid for medical expenses prior to Hospitalisation, and

c) expenses paid for medical expenses after discharge from Hospital Shall not exceed the Sum

Insured.

The Sum Insured under the policy is available for any or all the members covered for one or more claims

during the tenure of the policy.

For Personal accident, the coverage will be as described under Section II of Q.4

18. CAN I GET TREATED ANYWHERE IN INDIA?

The Policy covers treatment only in India. Even within India, if premium is paid for lower Zone and

treatment taken in higher Zone, our liability towards any claim will be 80% of admissible claim amount or

Sum Insured, whichever is less. Zone Classification is given below.

Illustration:

1) Insured XYZ, Sum Insured: Rs. 200000, Zone Selected: Zone III

Admissible Claim: Rs. 80000, Treatment taken in: Zone II

In such case Our liability will be 80% of the admissible claim amount i.e. Rs. 64000 (80% of Rs. 80000). Rest

of the amount will be borne by the Insured i.e. Rs. 16000.

2) Insured ABC, Sum Insured: Rs. 200000, Zone Selected: Zone II

Admissible Claim: Rs. 300000, Treatment taken in: Zone I

In such case, our liability will be 80% of admissible claim amount i.e. Rs. 240000 (80% of Rs. 300000). But

the claim amount cannot exceed the Sum Insured viz. Rs. 200000. Thus our total liability will be Rs. 200000.

UIN: NIAHLIP24123V032324 Page 16 of 24

NEW INDIA ASHA KIRAN POLICY

Note: Co-pay will not be applied on the Sum Insured, it is always applicable on the admissible claim

amount.

Zone- I

Greater Mumbai (includes Mira-Bhayandar, Thane, Navi Mumbai, Kalyan-Dombivli,

Ulhasnagar, Ambarnath, Badlapur) and State of Gujarat

Zone-II

Delhi NCR (includes Faridabad, Gurgaon, Mewat, Rohtak, Sonepat, Rewari, Jhajjhar,

Panipat and Palwal, Meerut, Ghaziabad, GautamBudha Nagar, Bulandshahr, and

Baghpat, Alwar and NCT of Delhi), Bangalore, Chennai, Hyderabad and

Secunderabad, Pune and Kolkata

Zone-III

Rest of India (other than those areas specified in Zone I and II)

The Cities mentioned below would include their Urban Agglomeration. The Insured Person can choose

the Zone at the time of proposal, and can also change it at the time of renewal. It is therefore in

your interest to choose the appropriate Zone and pay the necessary premium depending upon

your preference for coverage.

19. WHAT SUM INSURED SHOULD I CHOOSE?

You are free to choose any Sum Insured from Rs. 2, 3, 5, 8, 10, 12 and 15 Lakhs. The premium payable is

determined based on the following criteria:

a. The premium for the eldest member of the family. (Premium from Primary Member Premium

Table)

b. Premium for All additional members to be covered in this policy. (Premium from Additional

Member Premium Table)

c. Premium for the daughter(s) shall be 50% of her premium from Additional Member Premium

Table.

d. Sum Insured

e. Zone

You are free to choose any Sum Insured available as specified above. But it is in your own interest to choose

the Sum Insured which could satisfy your present as well as future needs.

20. HOW LONG IS THE POLICY VALID?

The Policy is valid during the Period of Insurance stated in the Schedule attached to the Policy. It is usually

valid for a period of one year from the date of beginning of insurance.

21. CAN THE POLICY BE RENEWED WHEN THE PRESENT POLICY EXPIRES?

Yes. You can and to get all Continuity benefits under the Policy, you should renew the Policy before the

expiry of the present policy. For instance, if Your Policy commences from 2nd October, 2021 date of expiry

is usually on 1st October, 2022. You should renew Your Policy by paying the Renewal Premium on or before

1st October 2022.

UIN: NIAHLIP24123V032324 Page 17 of 24

NEW INDIA ASHA KIRAN POLICY

The Company, with prior approval of lRDAl, may withdraw, revise or modify the terms of the policy

including the premium rates. The insured person shall be notified three months before the changes are

effected.

You can choose to migrate to any of our existing Policy, subject to Regulations of IRDAI (Protection of

Policyholders’ Interest) Regulations, 2017 and the Guidelines of IRDAI on Portability and Migration of

Health Insurance Policies, as amended from time to time.

Please note that:

i. The Company shall endeavor to give notice for renewal. However, the Company is not under

obligation to give any notice for renewal.

ii. Renewal shall not be denied on the ground that the insured person had made a claim or claims in

the preceding policy years.

iii. Request for renewal along with requisite premium shall be received by the Company before the end

of the policy period.

iv. At the end of the policy period, the policy shall terminate and can be renewed within the Grace

Period of 30 days to maintain continuity of benefits without break in policy. Coverage is not available

during the Grace Period.

v. No loading shall apply on renewals based on individual claims experience.

22. WHAT IS CONTINUITY BENEFIT?

There are certain treatments which are payable only after the Insured Person is continuously covered for

a specified period. For example, Cataract is covered only after twenty-four months of Continuous Coverage.

If an Insured took a Policy in October, 2019, does not renew it on time and takes a Policy only in December

2020, and renewed it on time in December 2021, any claim for Cataract would not become payable,

because the Insured Person was not continuously covered for twenty-four months. If, he had renewed the

Policy in time in October 2020 and then in October 2021, then he would have been continuously covered

for twenty-four months and therefore his claim for Cataract in the Policy beginning from October 2021

would be payable. Therefore, you should always ensure that you pay your renewal Premium before Your

Policy expires.

23. IS THERE ANY GRACE PERIOD FOR RENEWAL OF THE POLICY?

Yes. If Your Policy is renewed within thirty days of the expiry of the previous Policy, then the Continuity

Benefits would not be affected. But even if You renew Your Policy within thirty days of expiry of previous

Policy, any Illness contracted or Injury sustained or Hospitalisation commencing during the break in

insurance is not covered. Therefore, it is in your own interest to see that you renew the Policy before it

expires.

24. CAN THE SUM INSURED BE INCREASED AT THE TIME OF RENEWAL?

Yes. You may seek enhancement of Sum Insured in writing before payment of premium for renewal, which

may be granted at Our discretion. Before granting such request for enhancement of Sum Insured, We have

the right to have You examined by a Medical Practitioner authorized by Us or the TPA (50% of Medical

examination cost will be reimbursed to the Insured Person). Our consent for enhancement of Sum Insured

is dependent on the recommendation of the Medical Practitioner.

Enhancement of Sum Insured shall be allowed based on the following table:

Age<=50 years

Enhancement up to Sum Insured of 15 lakhs without Medical Examination.

Age 51-60 Years

Enhancement by two slabs without Medical Examination

Age 51-60 Years

Enhancement up to 15 Lakhs with Medical Examination

Age 61-65 Years

Enhancement by one slab with Medical Examination

UIN: NIAHLIP24123V032324 Page 18 of 24

NEW INDIA ASHA KIRAN POLICY

Enhancement of Sum Insured will not be considered for:

1) Insured Persons over 65 years of age.

2) Insured Person who had undergone Hospitalization in the preceding two years.

3) Insured Persons suffering from one or more of the following Illnesses/Conditions:

i Any chronic Illness/ Ailment

ii Any recurring Illness/ Ailment

iii Any Critical Illness

In respect of any increase in Sum Insured, exclusion 4.1, 4.2, 4.3 would apply to the additional Sum Insured

from the date of such increase.

25. IS THERE AN AGE LIMIT UPTO WHICH THE POLICY WOULD BE RENEWED?

No. Your Policy can be renewed, as long as you pay the Renewal Premium before the date of expiry of the

Policy. There is an age limit for taking a fresh Policy, but there is no age limit for renewal.

Children between 18 years to 25 years can be continue to be covered in the Policy provided they are

financially dependent on the parents and one or both parents are covered simultaneously. On attaining the

age of 18 years or ceasing to be financially dependent on the parents, they can, on renewal take a separate

Policy. In such an event the benefits on Continuous Coverage can be ported to the new Policy. The upper

age limit will not apply to a mentally challenged children and an unmarried dependent daughter(s).

If you do not renew Your Policy before the date of expiry or within thirty days of the date of expiry, the

Policy may not be renewed, and only a fresh Policy could be issued, subject to our underwriting rules. In

such cases, it is possible that a fresh Policy could not be issued by us. It is therefore in your interest to

ensure that Your Policy is renewed before expiry.

26. CAN THE INSURANCE COMPANY REFUSE TO RENEW THE POLICY?

We may refuse to renew the Policy only on rare occasions such as fraud, misrepresentation or non-

disclosure of material facts or non-cooperation being committed by You or any one acting on Your behalf

in obtaining insurance or subsequently in relation thereto. If we discontinue selling this Policy, it might not

be possible to renew this Policy on the same terms and conditions. In such a case you shall, however, have

the option for renewal under any similar Policy being issued by the Company, provided the benefits payable

shall be subject to the terms contained in such other Policy.

27. CAN I MAKE A CLAIM IMMEDIATELY AFTER TAKING A POLICY?

Claims for Illnesses cannot be made during the first thirty days of a fresh Insurance policy. However, claims

for Hospitalisation due to accidents occurring even during the first thirty days are payable. There are certain

treatments where the waiting period is 90 days, two years or four years.

28. WHAT IS THIRD PARTY ADMINISTRATOR (TPA)?

Third Party Administrator (TPA) is a service provider to facilitate service to you for providing Cashless facility

for all Hospitalisation that come under the scope of the policy. The TPA also settles reimbursement claims

within the scope of the Policy.

29. WHAT IS CASHLESS HOSPITALISATION?

Cashless Hospitalisation is service provided by the TPA on Our behalf whereby you are not required to

settle the Hospitalisation expenses at the time of discharge from Hospital. The settlement is done directly

by the TPA on Our behalf. However, those expenses which are not admissible under the Policy would not

be paid and you would have to pay such inadmissible expenses to the Hospital. Cashless facility is available

only in Networked Hospitals. Prior approval is required from the TPA before the patient is admitted into

the Networked Hospital. You may visit our Website at http://newindia.co.in/listofhospitals.aspx. The list of

UIN: NIAHLIP24123V032324 Page 19 of 24

NEW INDIA ASHA KIRAN POLICY

Networked Hospitals can also be obtained from the TPA or from their website. You will have full freedom

to choose the hospitals from the Networked Hospitals and avail Cashless facility on production of proof of

Insurance and Your identity, subject to the claim being admissible. The TPA might not agree to provide

Cashless facility at a Hospital which is not a Network Hospital. In such cases you may avail treatment at any

Hospital of Your choice and seek reimbursement of the claim subject to the terms and conditions of the

Policy. In cases where the admissibility of the claim could not be determined with the available documents,

even if the treatment is at a Network Hospital, the TPA may refuse to provide Cashless facility. Such refusal

may not necessarily mean denial of the claim. You may seek reimbursement of the expenses incurred by

producing all relevant documents and the TPA may pay the claim, if it is admissible under the terms and

conditions of the Policy.

30. CAN I CHANGE HOSPITALS DURING THE COURSE OF MY TREATMENT?

Yes, it is possible to shift to another hospital for reasons of requirement of better medical procedure.

However, this will be evaluated by Us / TPA on the merits of the case and as per policy terms and conditions.

31. HOW TO GET REIMBURSEMENTS IN CASE OF TREATMENT IN NON- NETWORK HOSPITALS OR DENIAL

OF CASHLESS FACILITY?

In case of treatment in a non-Network Hospital, TPA will reimburse You the amount of bills subject to the

conditions of the Policy. You must ensure that the Hospital where treatment is taken fulfills the conditions

of definition of Hospital in the Policy. Within twenty-four hours of Hospitalisation the TPA should be

intimated.

32. HOW TO GET REIMBURSEMENT FOR PRE AND POST HOSPITALISATION EXPENSES?

The Policy allows reimbursement of medical expenses incurred before and after admissible Hospitalisation

up to a certain number of days. For reimbursement, send all bills in original with supporting documents

along with a copy of the discharge summary and a copy of the authorization letter to his/her

TPA/underwriting office, whichever applicable. The bills must be sent to the TPA/underwriting office within

15 days from the date of completion of treatment. You must also provide the TPA/underwriting office with

additional information and assistance as may be required by the Company/TPA in dealing with the claim.

33. WILL THE ENTIRE AMOUNT OF THE CLAIMED EXPENSES BE PAID?

The entire amount of the claim is payable, if it is within the Sum Insured and is related with the

Hospitalisation as per Policy conditions and is supported by proper documents, except the expenses which

are excluded.

Personal Accident claims will be paid as mentioned Point 5 –Section II, without any deductions.

Hospitalisation cover is independent of Personal Accident cover. Upon happening of accident if the Insured

Person is Hospitalised, Hospitalisation will be paid in addition to compensation being paid under Personal

Accident coverage.

34. CAN ANY CLAIM BE REJECTED OR REFUSED?

Yes. A claim, which is not covered under the Policy conditions, can be rejected. Claims may also be rejected

in the event of misrepresentation, misdescription or nondisclosure of any material fact/particular. ln case

of any grievance the insured person may contact the company through

Website: https://www.newindia.co.in/portal/readMore/Grievances

Toll free: 1800-209-1415

E-mail, Fax and Courier: As mentioned in the above address

Senior Citizens may write to seniorcitizencare.ho@newindia.co.in

lnsured person may also approach the grievance cell at any of the company's branches with the details of

grievance.

UIN: NIAHLIP24123V032324 Page 20 of 24

NEW INDIA ASHA KIRAN POLICY

lf lnsured person is not satisfied with the redressal of grievance through one of the above methods, insured

person may contact the grievance officer at https://www.newindia.co.in/portal/readMore/Grievances For

updated details of grievance officer, kindly refer the link

https://www.newindia.co.in/portal/readMore/Grievances

lf lnsured person is not satisfied with the redressal of grievance through above methods, the insured person

may also approach the office of lnsurance Ombudsman of the respective area/region for redressal of

grievance as per lnsurance Ombudsman Rules 2017. Please refer to Annexure III of the Policy Clause.

Grievance may also be lodged at IRDAI lntegrated Grievance Management System - https://igms.

irdai.gov.in

35. CAN I CANCEL THE POLICY?

The policyholder may cancel this policy by giving 15 days written notice and in such an event, the Company

shall refund premium for the unexpired policy period at Our short period rate detailed below.

Period On Risk

Rate of Premium To Be Charged

(Retained By The Insurer)

Up to one month

1/4th of the annual rate

Up to three months

1/2 of the annual rate

Up to six months

3/4th of the annual rate

Exceeding six months

Full annual rate

In the event of death of insured in the middle of policy year/during the course of policy period, the premium

for the unexpired policy period shall be refunded proportionately.

Notwithstanding anything contained herein or otherwise, no refunds of premium shall be made in respect

of Cancellation where, any claim has been admitted or has been lodged or any benefit has been availed by

the insured person under the policy.

The Company may cancel the policy at any time on grounds of misrepresentation non-disclosure of material

facts, fraud by the insured person by giving 15 days' written notice. There would be no refund of premium

on cancellation on grounds of misrepresentation, non-disclosure of material facts or fraud.

36. WHAT IS FREE LOOK PERIOD?

The Free Look Period shall be applicable on new individual health insurance policies and not on renewals

or at the time of porting/migrating the policy.

The insured person shall be allowed free look period of fifteen days from date of receipt of the policy

document to review the terms and conditions of the policy, and to return the same if not acceptable.

lf the insured has not made any claim during the Free Look Period, the insured shall be entitled to

i. a refund of the premium paid less any expenses incurred by the Company on medical examination

of the insured person and the stamp duty charges or

ii. where the risk has already commenced and the option of return of the policy is exercised by the

insured person, a deduction towards the proportionate risk premium for period of cover or

iii. Where only a part of the insurance coverage has commenced, such proportionate premium

commensurate with the insurance coverage during such period;

37. IS THERE ANY BENEFIT UNDER THE INCOME TAX ACT FOR THE PREMIUM PAID FOR THIS INSURANCE?

Yes. Payments made for health insurance in any mode other than cash are eligible for deduction from

taxable income as per Section 80 D of the Income Tax Act, 1961. For details, please refer to the relevant

Section of the Income Tax Act.

UIN: NIAHLIP24123V032324 Page 21 of 24

NEW INDIA ASHA KIRAN POLICY

38. IF THE CLAIM EVENT FALLS WITHIN TWO POLICY PERIODS, HOW MUCH WILL BE PAID?

If the claim event falls within two policy periods, the claims shall be paid taking into consideration the

available Sum Insured of the expiring Policy only. Sum Insured of the Renewed Policy will not be available

for the Hospitalisation (including Pre & Post Hospitalisation Expenses), which has commenced in the

expiring Policy. Claim shall be settled on per event basis.

39. WHAT WILL HAPPEN TO THE POLICY WHEN THE DAUGHTER/S BECOMES FINANCIALLY DEPENDENT OR

A BOY CHILD IS BORN AFTER TAKING THE POLICY?

The Company shall offer an option to migrate to suitable Health Insurance policy once the Daughter/s

become financially independent or a Boy child is born after taking the policy.

UIN: NIAHLIP24123V032324 Page 22 of 24

NEW INDIA ASHA KIRAN POLICY

New India Asha Kiran Policy - Premium Chart (Excluding GST)

Sum

Insured

Zone

PRIMARY MEMBER Premiums applicable at different ages

(Rs. per annum excluding GST)

0-20 Y

21-30 Y

30-35 Y

36-40 Y

41-45 Y

46-50 Y

51-55 Y

56-60 Y

61-65 Y

2,00,000

I

2,930

3,986

4,742

5,813

7,545

9,215

12,869

15,750

26,555

3,00,000

I

4,087

5,396

6,086

7,424

9,643

11,775

17,111

20,903

35,339

5,00,000

I

5,829

7,917

8,914

10,907

12,667

15,479

23,287

28,474

48,348

8,00,000

I

7,157

9,715

10,950

13,394

15,562

19,001

28,590

35,507

59,359

10,00,000

I

8,170

11,096

12,493

15,286

17,753

21,694

32,637

39,645

67,316

12,00,000

I

8,882

12,063

13,582

16,618

19,300

23,585

35,481

43,040

73,082

15,00,000

I

10,069

13,675

15,397

18,840

21,880

26,737

40,223

48,705

82,700

Sum

Insured

Zone

0-20 Y

21-30 Y

30-35 Y

36-40 Y

41-45 Y

46-50 Y

51-55 Y

56-60 Y

61-65 Y

2,00,000

II

2,663

3,623

4,316

5,277

6,852

8,379

11,703

14,318

24,146

3,00,000

II

3,720

4,910

5,527

6,748

8,761

10,702

15,553

19,008

32,120

5,00,000

II

5,296

7,194

8,108

9,910

11,521

14,074

21,172

25,880

43,953

8,00,000

II

6,502

8,833

9,954

12,172

14,150

17,275

25,994

32,281

53,966

10,00,000

II

7,423

10,083

11,364

13,889

16,146

19,725

29,673

36,034

61,196

12,00,000

II

8,069

10,961

12,354

15,099

17,553

21,443

32,258

39,120

66,438

15,00,000

II

9,148

12,426

14,005

17,117

19,899

24,310

36,570

44,269

75,182

Sum

Insured

Zone

0-20 Y

21-30 Y

30-35 Y

36-40 Y

41-45 Y

46-50 Y

51-55 Y

56-60 Y

61-65 Y

2,00,000

III

2,394

3,261

3,891

4,757

6,174

7,545

10,538

12,884

21,735

3,00,000

III

3,352

4,425

4,969

6,072

7,879

9,629

13,994

17,111

28,916

5,00,000

III

4,765

6,470

7,303

8,914

10,374

12,667

19,055

23,287

39,558

8,00,000

III

5,846

7,951

8,959

10,962

12,739

15,548

23,399

29,056

48,574

10,00,000

III

6,678

9,068

10,236

12,493

14,539

17,753

26,707

32,423

55,077

12,00,000

III

7,259

9,858

11,128

13,582

15,806

19,300

29,034

35,200

59,794

15,00,000

III

8,230

11,176

12,615

15,397

17,919

21,880

32,914

39,833

67,664

UIN: NIAHLIP24123V032324 Page 23 of 24

NEW INDIA ASHA KIRAN POLICY

Sum

Insured

Zone

ADDITIONAL MEMBER Premiums applicable at different ages

(Rs. per annum excluding GST)

0-20 Y

21-30 Y

30-35 Y

36-40 Y

41-45 Y

46-50 Y

51-55 Y

56-60 Y

61-65 Y

2,00,000

I

395

567

804

977

1,733

2,111

4,473

5,466

17,262

3,00,000

I

545

764

1,000

1,235

2,220

2,720

5,925

7,248

22,947

5,00,000

I

779

1,134

1,489

1,816

2,908

3,563

8,068

9,870

31,409

8,00,000

I

958

1,386

1,828

2,231

3,578

4,373

9,892

12,109

38,556

10,00,000

I

1,091

1,589

2,086

2,545

4,076

4,994

11,307

13,742

43,732

12,00,000

I

1,186

1,727

2,268

2,767

4,431

5,429

12,292

14,919

47,477

15,00,000

I

1,345

1,958

2,571

3,137

5,023

6,155

13,935

16,882

53,726

Sum

Insured

Zone

0-20 Y

21-30 Y

30-35 Y

36-40 Y

41-45 Y

46-50 Y

51-55 Y

56-60 Y

61-65 Y

2,00,000

II

363

521

725

882

1,575

1,922

4,064

4,962

15,687

3,00,000

II

500

692

911

1,117

2,015

2,470

5,380

6,586

20,860

5,00,000

II

710

1,024

1,352

1,652

2,648

3,236

7,331

8,969

28,556

8,00,000

II

870

1,260

1,663

2,029

3,251

3,970

8,996

11,012

35,053

10,00,000

II

995

1,436

1,895

2,316

3,711

4,535

10,274

12,487

39,759

12,00,000

II

1,081

1,561

2,060

2,518

4,035

4,930

11,169

13,557

43,164

15,00,000

II

1,226

1,769

2,335

2,854

4,574

5,589

12,662

15,341

48,845

Sum

Insured

Zone

0-20 Y

21-30 Y

30-35 Y

36-40 Y

41-45 Y

46-50 Y

51-55 Y

56-60 Y

61-65 Y

2,00,000

III

332

473

647

788

1,418

1,733

3,654

4,473

14,112

3,00,000

III

456

617

823

1,000

1,809

2,220

4,837

5,925

18,773

5,00,000

III

642

928

1,216

1,489

2,389

2,908

6,594

8,068

25,704

8,00,000

III

781

1,134

1,500

1,828

2,923

3,578

8,102

9,917

31,550

10,00,000

III

900

1,301

1,704

2,086

3,349

4,076

9,241

11,233

35,787

12,00,000

III

978

1,414

1,852

2,268

3,641

4,431

10,046

12,195

38,853

15,00,000

III

1,109

1,603

2,100

2,571

4,127

5,023

11,389

13,800

43,966

Premium will increase by 2% for every year after the age of 65 years for both Primary and Additional

members.

UIN: NIAHLIP24123V032324 Page 24 of 24

NEW INDIA ASHA KIRAN POLICY

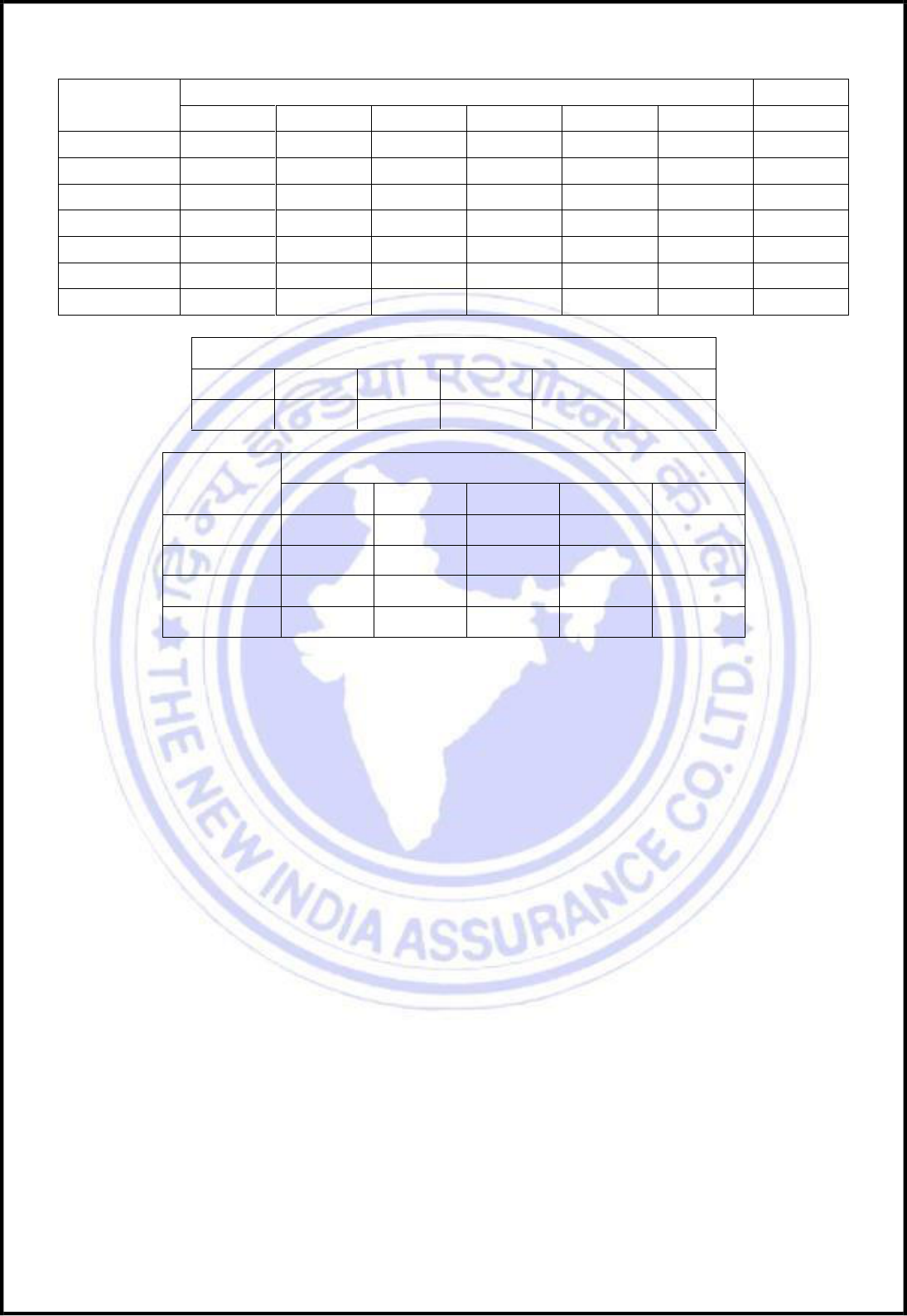

Optional Covers – Per Member Premium (Excluding GST)

Sum Insured

(Rs.)

OPTIONAL COVER I : NO PROPORTIONATE DEDUCTION

<35

36-45

46-50

51-55

56-60

61-65

>65

2,00,000

1,418

1,506

2,483

3,741

4,852

6,419

9,201

3,00,000

980

1,040

1,715

2,584

3,351

4,434

6,355

5,00,000

770

817

1,348

2,031

2,634

3,485

4,995

8,00,000

646

686

1,131

1,704

2,210

2,924

4,191

10,00,000

662

703

1,159

1,747

2,265

2,997

4,296

12,00,000

644

684

1,127

1,699

2,203

2,915

4,178

15,00,000

458

487

802

1,209

1,568

2,075

2,974

OPTIONAL COVER II : MATERNITY EXPENSES BENEFIT

SI

5,00,000

8,00,000

10,00,000

12,00,000

15,00,000

(Rs.)

5,000

8,000

10,000

12,000

15,000

Sum Insured

(Rs.)

OPTIONAL COVER III : REVISION IN LIMIT OF CATARACT

<50

51-55

56-60

61-65

>65

8,00,000

444

1,049

2,269

3,645

3,893

10,00,000

555

1,311

2,836

4,556

4,866

12,00,000

666

1,573

3,404

5,467

5,839

15,00,000

832

1,967

4,255

6,834

7,299

Optional Cover IV: For Non-Medical Items (Consumables): This optional cover is for covering medical consumables (Non-Payable items).

It is applicable for Sum Insured of 8 L & above, and is payable up to a maximum of Rs. 15,000 per policy period. The premium charged for

this add on cover will be rated Rs 1500/- per member.